-Analysis-

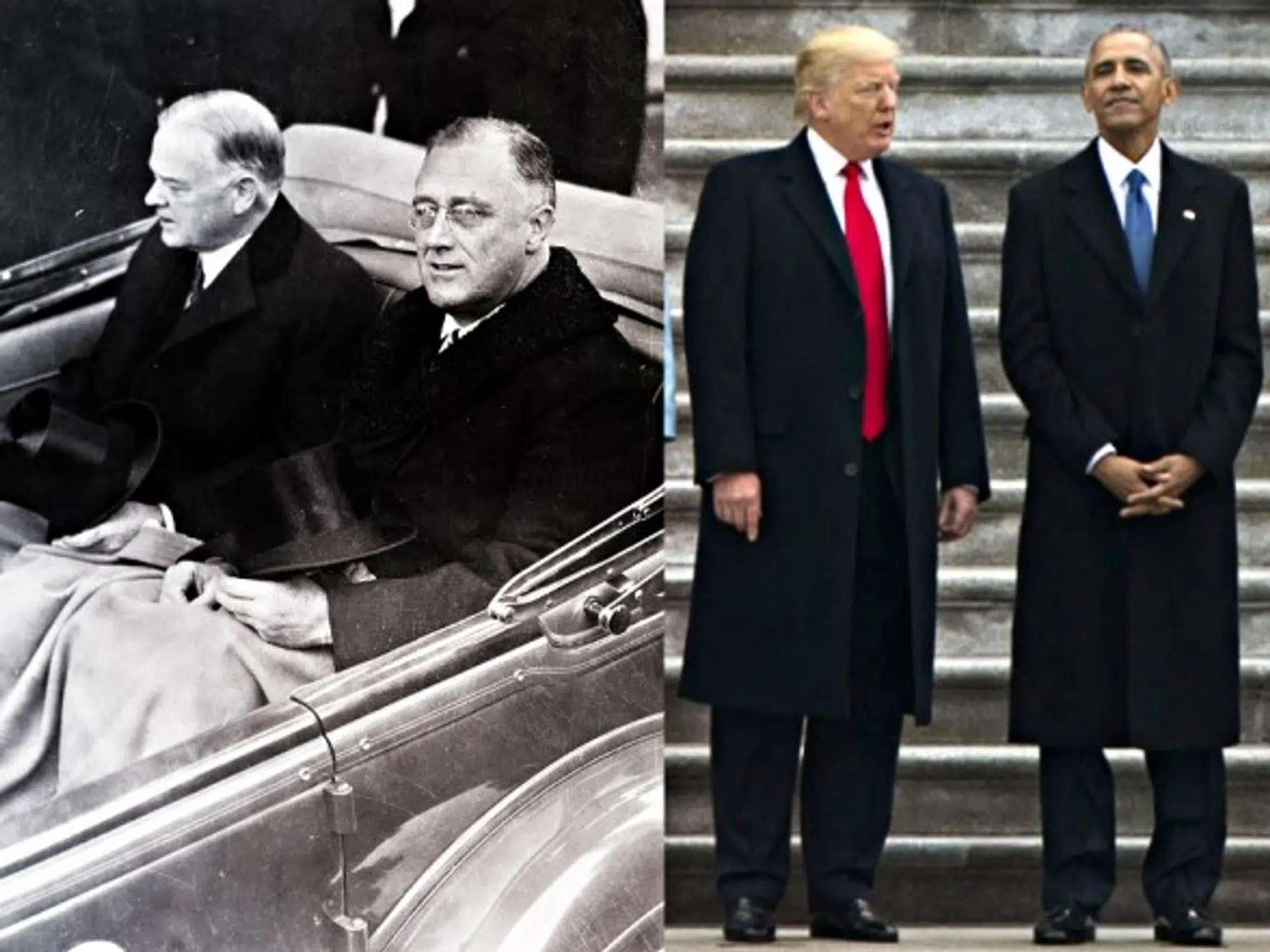

The marker of the “First 100 Days’ of a new presidency traces its origins to Franklin Roosevelt’s arrival in the White House in 1933, when the Democratic president followed through on a series of promised measures to urgently reverse the economic policies of his predecessor, the hapless Herbert Hoover. This initial policy sprint would not only help pull the country out of the Great Depression, but would eventually be cemented into the New Deal, a thorough rewriting of the socio-economic contract of the government of the United States with its citizenry.

By all accounts, President Donald Trump is operating with the same haste, hoping to cash in on the supposed political capital that comes with having just been democratically elected. In his first 10 days in office, Trump has signed a series of executive orders to ban immigrants from seven Muslim-majority countries, build a wall on the border with Mexico and implement a blatantly protectionist trade policy. On some level, no one should be surprised: Trump was simply following through on the promises that were the heart of an electoral campaign that got him elected — and no doubt his core supporters are thrilled that the billionaire real estate mogul is turning out to be a man of his word.

But there are millions of supporters not of the diehard variety, who saw Trump as the lesser of two evils, who would take the country more in direction A than direction B. These were the people who were said to take his often shocking campaign “seriously but not literally.” Now that we are heading full-speed in Direction X, what will they think? More than his core supporters at home or the throngs of opponents protesting in the streets, it is the reluctant Trump voter who will determine whether these first 100 days are a footnote in history or the beginning of a whole new chapter.